Contents

はじめに

ある程度投資を行っていくと銘柄の選定,買い時や売り時の判断のために自分で株価データを自由に扱いたいというニーズが出てくると思います。この記事では,Yahoo Financeのページから自分が知りたい銘柄の時系列株価データをダウンロードする方法を紹介します。

この記事を読むことで,

MATLABを使用してYahoo Financeから自分の好きな銘柄の時系列株価データをダウンロードすることができます!

File Exchangeの活用

MATLABはユーザーコミュニティが充実していて,その特徴的なもののひとつにFile Exchange という場があります。File Exchangeは,ユーザーが自作した関数やアプリなどを共有していて,世界中のMATLABユーザーの英知が結集された夢のような場所です。今回は,その世界中の優秀なMATLABユーザーから,株価データを取得するお知恵を拝借します。ダウンロード数も多く高評価レビューも多そうだったのでこちらのJosiah Renfree氏の作成したhist_stock_data関数を使用させてもらいます。ダウンロードボタンからm fileと関連するドキュメントをダウンロードすることができます。

それでは早速コードの中身を見ていきます。2行目からのコメントで使い方を詳しく書いてくださっています。銘柄の指定方法や取得データの間隔(日次か週次かなど)などでいくつかのオプションがありますが,3行目で明記されている株価取得の開始日(X)と終了日(Y),銘柄(Ticker)を引数で渡すパターンが一番シンプルかと思いますので,その例でデータを取得してみます。実際のデータ取得に関わる部分のコード(146行目あたりから)を見てみるとやっていることはとてもシンプルで,引数で指定した期間,銘柄のデータをYahoo FinanceのHistorical Dataからダウンロードしています。

function stocks = hist_stock_data(start_date, end_date, varargin)

% HIST_STOCK_DATA Obtain historical stock data

% hist_stock_data(X,Y,'Ticker1','Ticker2',...) retrieves historical stock

% data for the ticker symbols Ticker1, Ticker2, etc... between the dates

% specified by X and Y. X and Y can either be strings in the format

% ddmmyyyy or Matlab datenums, where X is the beginning date and Y is the

% ending date. The program returns the stock data in a structure giving

% the Date, Open, High, Low, Close, Volume, and Adjusted Close price

% adjusted for dividends and splits.

%

% hist_stock_data(X,Y,'tickers.txt') retrieves historical stock data

% using the ticker symbols found in the user-defined text file. Ticker

% symbols must be separated by line feeds.

%

% hist_stock_data(X,Y,{'Ticker1' 'Ticker2'}) combined the ticker symbols

% into a single cell array when calling hist_stock_data (sometimes easier

% for calling the funtion with a cell array of ticker symbols).

%

% hist_stock_data(X,Y,'Ticker1','frequency',FREQ) retrieves historical

% stock data using the frequency specified by FREQ, which must be either

% 'd' for daily, 'wk' for weekly, or 'mo' for monthly.

%

% hist_stock_data(X,Y,'Ticker1','type','div') retrieves dividend data. If

% anything but 'div' is specified then it will default to retrieving

% historical prices.

%

% EXAMPLES

% stocks = hist_stock_data('23012003','15042008','GOOG','C');

% Returns the structure array 'stocks' that holds historical

% stock data for Google and CitiBank for dates from January

% 23, 2003 to April 15, 2008.

%

% stocks = hist_stock_data('12101997','18092001','tickers.txt');

% Returns the structure arrary 'stocks' which holds historical

% stock data for the ticker symbols listed in the text file

% 'tickers.txt' for dates from October 12, 1997 to September 18,

% 2001. The text file must be a column of ticker symbols

% separated by new lines.

%

% stocks = hist_stock_data(now-10, now, {'GOOG' 'C'});

% Get stock data for approximately the last 10 days for the two

% tickers specified in the cell array.

%

% stocks = hist_stock_data('12101997','18092001','C','frequency','w')

% Returns historical stock data for Citibank using the date range

% specified with a frequency of weeks. Possible values for

% frequency are d (daily), wk (weekly), or mo (monthly). If not

% specified, the default frequency is daily.

%

% stocks = hist_stock_data('12101997','18092001','C','type','div')

% Returned historical dividend data for Citibank between Oct 12,

% 1997 and September 18, 2001.

%

% DATA STRUCTURE

% INPUT DATA STRUCTURE FORMAT

% X (start date) ddmmyyyy String

% Y (end date) ddmmyyyy String

% Ticker NA String

% ticker.txt NA Text file

% FREQ NA String; 'd', 'wk', or 'mo'

% TYPE NA String; 'div'

%

% OUTPUT FORMAT

% All data is output in the structure 'stocks'. Each structure

% element will contain the ticker name, then vectors consisting of

% the organized data sorted by date, followed by the Open, High, Low,

% Close, Volume, then Adjusted Close prices.

%

% DATA FEED

% The historical stock data is obtained using Yahoo! Finance website.

% By using Yahoo! Finance, you agree not to redistribute the

% information found therein. Therefore, this program is for personal

% use only, and any information that you obtain may not be

% redistributed.

%

% NOTE

% This program uses the Matlab command urlread in a very basic form.

% If the program gives you an error and does not retrieve the stock

% information, it is most likely because there is a problem with the

% urlread command. You may have to tweak the code to let the program

% connect to the internet and retrieve the data.

% Created by Josiah Renfree

% January 25, 2008

stocks = struct([]); % initialize data structure

%% Parse inputs

% Format start and end dates into Posix times. This is the number of

% seconds since Jan 1, 1970. This previously used the posixtime function,

% but since that is relatively new, it now does the calculation using

% Matlab datenum's, which are in units of days, then converting to seconds.

origDate = datenum('01-Jan-1970 00:00:00', 'dd-mmm-yyyy HH:MM:SS');

% Convert input dates to Matlab datenums, if necessary

if ischar(start_date)

startDate = (datenum(start_date, 'ddmmyyyy') - origDate) * 24 * 60 * 60;

else

startDate = (floor(start_date) - origDate) * 24 * 60 * 60;

end

if ischar(end_date)

endDate = (datenum(end_date, 'ddmmyyyy') - origDate) * 24 * 60 * 60;

else

endDate = (floor(end_date) - origDate) * 24 * 60 * 60;

end

% determine if user specified frequency

temp = find(strcmp(varargin,'frequency') == 1); % search for frequency

if isempty(temp) % if not given

freq = 'd'; % default is daily

else % if user supplies frequency

freq = varargin{temp+1}; % assign to user input

varargin(temp:temp+1) = []; % remove from varargin

end

clear temp

% determine if user specified event type

temp = find(strcmp(varargin,'type') == 1); % search for frequency

if isempty(temp) % if not given

event = 'history'; % default is historical prices

else % if user supplies frequency

event = varargin{temp+1}; % assign to user input

varargin(temp:temp+1) = []; % remove from varargin

end

clear temp

% If the first cell of varargin is itself a cell array, assume it is a cell

% array of ticker symbols

if iscell(varargin{1})

tickers = varargin{1};

% Otherwise, check to see if it's a .txt file

elseif ~isempty(strfind(varargin{1},'.txt'))

fid = fopen(varargin{1}, 'r');

tickers = textscan(fid, '%s'); tickers = tickers{:};

fclose(fid);

% Otherwise, assume it's either a single ticker or a list of tickers

else

tickers = varargin;

end

%% Get historical data

h = waitbar(0, 'Please Wait...'); % create waitbar

idx = 1; % idx for current stock data

% Cycle through each ticker symbol and retrieve historical data

for i = 1:length(tickers)

% Update waitbar to display current ticker

waitbar((i-1)/length(tickers), h, ...

sprintf('Retrieving stock data for %s (%0.2f%%)', ...

tickers{i}, (i-1)*100/length(tickers)))

% Create url string for retrieving data

url = sprintf(['https://query1.finance.yahoo.com/v7/finance/download/', ...

'%s?period1=%d&period2=%d&interval=1%s&events=%s'], ...

tickers{i}, startDate, endDate, freq, event);

% Create webread options variable to specify UserAgent

options = weboptions('UserAgent', 'Mozilla/5.0');

% Try to download stock data. Put in try/catch block in case it fails

try

temp = webread(url, 'matlabstockdata@yahoo.com', 'historical stocks',...

options);

% If data retrieval fails, skip to next ticker

catch

continue

end

% Write ticker symbol

stocks(idx).Ticker = tickers{i};

% Put data into appropriate variables

if strcmp(event, 'history') % If historical prices

stocks(idx).Date = temp.Date;

stocks(idx).Open = temp.Open;

stocks(idx).High = temp.High;

stocks(idx).Low = temp.Low;

stocks(idx).Close = temp.Close;

stocks(idx).AdjClose = temp.AdjClose;

stocks(idx).Volume = temp.Volume;

else % If dividends

stocks(idx).Date = temp.Date;

stocks(idx).Dividend = temp.Dividends;

end

% Increment stock index

idx = idx + 1;

% update waitbar

waitbar(i/length(tickers),h)

end

close(h) % close waitbarYahoo Finance から株価データをダウンロードする

Googleの株価データをダウンロードしてみる

株価の取得開始日と終了日,GoogleのTickerの 'GOOG'を引数として渡してあげます。2005年12月31日から2023年9月30日までのデータを取得してみます。

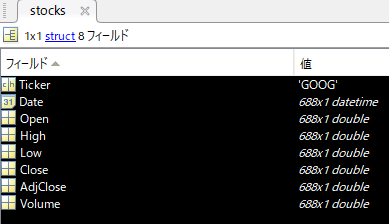

stocks = hist_stock_data('31122005','30092023','GOOG');実行結果

stocks の中身はこんな感じです。Dateは,日付情報,Openが始値,Highが高値,Lowが安値,Closeが終値,AdjCloseは調整後終値,Volumeが出来高です。

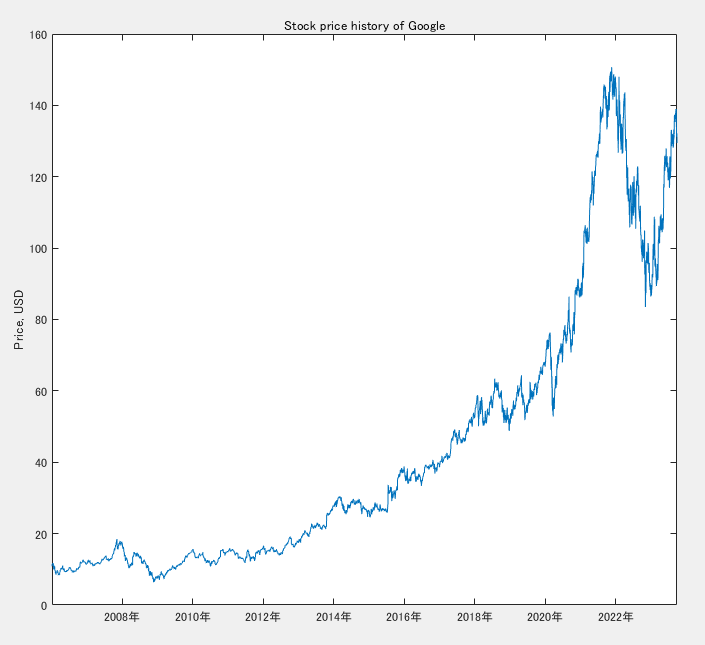

試しに終値をプロットしてみます。

plot(stocks.Date,stocks.AdjClose)

ylabel('Price, USD')

title('Stock price history of Google')

これで無事に,自分の手元で株価データを自由に扱えるようになりました。

日本株の場合は「証券コード.T」

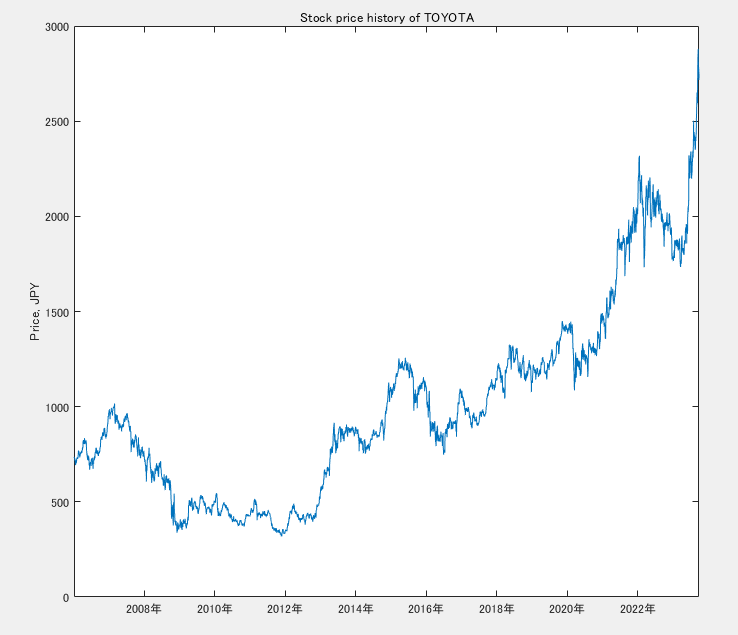

日本株のデータを取得したい場合は,Tickerを「証券コード.T」とすれば取得することができます。試しにトヨタ自動車の同期間の株価を取得してみましょう。トヨタ自動車の証券コードは,7203なので,Tickerを「7203.T」とします。

stocks = hist_stock_data('31122005','30092023','7203.T');

plot(stocks.Date,stocks.AdjClose)

ylabel('Price, JPY')

title('Stock price history of TOYOTA')実行結果

無事に取得することができました。

まとめ

この記事では,MATLAB File Exchanger で公開されている関数を使用して,自分の好きな銘柄の時系列株価データをYahoo Financeから取得する方法を紹介しました。銘柄指定の自由度が高く,操作もシンプルなJosiah Renfree氏の作成したhist_stock_data関数はおすすめです。